Normal Distribution

Description

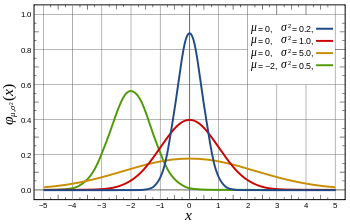

In probability theory, the normal (or Gaussian) distribution is a very commonly occurring continuous probability distribution—a function that tells the probability that any real observation will fall between any two real limits or real numbers, as the curve approaches zero on either side. According to the central limit theorem, under mild conditions, the mean of many random variables independently drawn from the same distribution is distributed approximately normally, irrespective of the form of the original distribution. A random variable with a Gaussian distribution is said to be normally distributed and is called a normal deviate.